At the same time Medicare came out with a prospective payment system (PPS) for LTACHs (see previous post) a similar new payment system was instituted for Inpatient Rehabilitation Facilities (IRFs). Under the old payment system, TEFRA reimbursed IRFs for the cost of care for Medicare patients. The payments were based on the allowed rehabilitation costs incurred, plus a small incentive to lower those costs each year. This cost reimbursement methodology under TEFRA was abandoned in favor of the new PPS installed for 2003. As with LTACHs, there was a three year phase-in option between TEFRA and PPS, which few providers chose, because the potential for profits was obvious with the PPS system.

Under the new system, a diagnosis was assigned upon admission, but the IRF also had three days to assign scores to the patient in a variety of functional areas, such as: other related diagnoses , mobility, feeding, self care, etc. A debilitated patient with say, a severe stroke would likely have a lower functional score than would a fairly healthy patient with an amputation. A lower score and more severe diagnosis would indicate the need for a longer stay and thus a higher potential payment for the IRF.

I am simplifying for the reader. Actually, rehab has a very complex set of regulations, which include functional scoring (FIM), change in FIM score at discharge, acuity (PAI) diagnostic grouping (CMG) discharge placement, outliers, etc. all of which affect Medicare payments. Also, patients must receive three minimum hours of therapy per day.

Additionally, a minimum of 60% of all patient admissions must be in 13 specific diagnostic categories. Got it? Patient R now passes though a variety of assessment tools by which payment is determined. But the level of impairment and the score improvements are determined by the IRF. Basically, the more impaired the patient, the higher the reimbursement. All in all, a well thought out but complicated methodology, with an underlying issue. The lower the admission scoring, the better the improvement scores, and the sooner a patient is discharged, the higher the potential IRF profit for that patient.

The current Medicare PPS incentives, as in LTACH, are to discharge patients as quickly as possible. But, in LTACH, there is a floor to early discharge, because the Average Length of Stay (ALOS) for all patients must be at least 25 days. However, in the rehab PPS, there is no real floor on ALOS, once the patient has been there for the 72 hours of assessment Let’s examine the results of this ingenious new reimbursement plan.

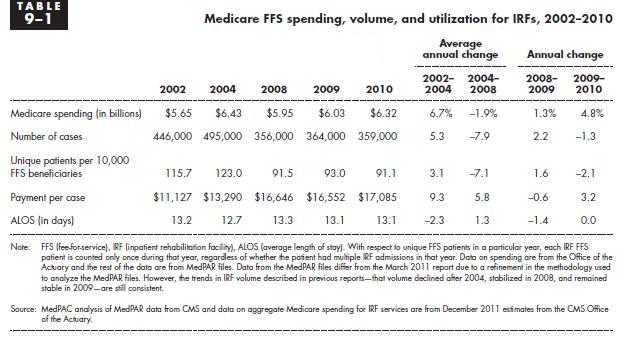

Under TEFRA in 2001, Medicare was paying $9952 per case. Under PPS, the payments ballooned to $17,085 in 2010, an increase of 72%, or over 39% in constant dollars. Not so good on cost control and saving those taxpayer dollars. This increase is magnified by the consideration that patient lengths of stay have also decreased by about 8% since PPS started. With PPS, Medicare pays more for less. Is this a good payment system?

Another unintended (perhaps) effect resulted. Under TEFRA, since Medicare was paying little more than cost, the profit margins had to come from private health insurers, who paid a higher rate than Medicare. But under PPS, the private insurers observed that since Medicare was paying out profits, the providers could be squeezed harder on the private rates. And squeezed they were. Now, many IRFs are being paid at or below costs by the private health insurers, exactly the opposite of TEFRA days!

So, the result of Medicare’s clever PPS payment plan is that taxpayers are paying for increased provider AND insurer profits. At the same time, patients are being discharged sooner. Their lengths of stay are now about 13 days, compared to 14 days in 2001 (and closer to 20 days in the mid nineties). I guess Medicare can trumpet the decreased LOS, but at what cost? I thought it was all about containing costs.

What was Medicare thinking?

source: MEDPAC